By Tim Buckley, December 16, 2019

Tim Buckley

Tim Buckley is director of energy finance studies at the Institute for Energy Economics and Financial Analysis, based in Sydney, Australia. He has 25 years of financial market experience covering the Australian, Asian and global equity markets from the perspectives of both the buy and sell side. Buckley was head of equity research at Citigroup, as well as co-managing director of Arkx Investment Management P/L, a global listed clean energy investment company jointly owned by management and the Westpac Banking Group.

Tim Buckley is director of energy finance studies at the Institute for Energy Economics and Financial Analysis, based in Sydney, Australia. He has 25 years of financial market experience covering the Australian, Asian and global equity markets from the perspectives of both the buy and sell side. Buckley was head of equity research at Citigroup, as well as co-managing director of Arkx Investment Management P/L, a global listed clean energy investment company jointly owned by management and the Westpac Banking Group.

In the often grim world of climate reporting, there is at least one upbeat story: India has been aggressively pivoting away from coal-fired power plants and towards electricity generated by solar, wind, and hydroelectric power. This means that the amount of carbon dioxide the country emits into the atmosphere should come down dramatically.

The reasons for this change are complex and interlocking, but one aspect in particular seems to stand out: The price for solar electricity has been in freefall, to levels so low they were once thought impossible. For example, since 2017, one solar energy company has been generating electricity in the Indian state of Rajasthan at the unheard-of, guaranteed wholesale price of 2.44 rupees per kilowatt-hour, or 3 US cents. (In comparison, the average price for electricity in the United States is presently about 13.19 cents per kilowatt-hour, and some locations in the country pay far more. As recently as 2008, the average homeowner on Block Island, Rhode Island, paid a staggering 61 cents per kilowatt-hour for electricity, before any other fees or charges—which can nearly double the price. And businesses had it even worse, with some business owners reporting electric bills of as much as $30,000 per month.)

Consequently, with this massive reduction in the cost of renewables, India is able to shift away from the world’s dirtiest fossil fuel, and to much cleaner sources. It’s a stunning change, and one that could have profound implications on the world energy market. While western countries continue to baulk at reducing their reliance on fossil fuels, India is accelerating its plans to lock in a sustained, aggressive reduction in the carbon emissions intensity of its economy. In fact, India’s prime minister, Narendra Modi, is targeting a fivefold expansion of the electricity generated from renewable energy sources by 2030—and this from a country that has already doubled its renewable energy in the past three years.

This means that India is committed to more than meeting the goals of its national contributions in the 2015 Paris Climate Agreement; it is going to “overdeliver,” in the parlance of economists. This development is all the more astonishing, because just a few years ago India was a villain when it came to coal use; in 2015, Modi’s ruling party had wanted to more than double India’s mining of coal, to 1.5 billion metric tons by 2020, despite the risks this posed to the climate and the country.

The benefits of this green sea-change are already being felt.

The rapid diversification of India’s electricity sector is creating an abundance of jobs and bringing an influx of new investment—needing to reach $500 billion over the coming decade if the targets are to be met—while reducing India’s emissions profile.

Ahead of the curve? Yes, India has certainly entered the global centre stage. Achievable? Entirely.

And this change of course also raises other questions, such as why India, and why now? What are the factors driving this energy transition from coal to renewables?

A perfect storm—in a good way. Several developments have come into play at once, that together have made for this startling, climate-friendly transformation of India’s energy policy. They can be generally categorized as coming from two camps; one environmental and one financial. On the environmental side, India had no choice but to deal with its poor air quality and water scarcity. On the financial end, unreliable power supplies—and India’s historic and growing dependence on imported fossil fuels—were an ongoing drag on its domestic economic growth.

We’ll take a look at each category in turn.

The environmental costs of increasing economic growth. Similar to China’s growth since the start of this century, India has been on an industrialization path that has pushed the country’s economy to grow at over 6 percent annually since 2010. In the coming decade, the Indian government is targeting 6-to-8 percent annual growth.

But such sustained economic growth comes with an ever-increasing environmental cost.

Take air pollution. Over the last couple of weeks, residents in the capital of New Delhi have likened their “hazardous” air quality to living in a gas chamber, while flights to the city have been diverted due to poor visibility, reported in the Australian Financial Review. In fact, a recent New York Times article used New Delhi as an example of some of the world’s worst air quality, noting that at 900 micrograms of fine particulates per cubic meter of air, the city was “blowing past the E.P.A.’s definition of ‘hazardous’ air (which maxes out at 500) and into extreme territory.” While seasonal factors are clearly at play, the deteriorating air quality is an all too powerful symbol of the growing environmental costs of strong economic growth for the people of India, and the right to breathe clean air is gaining traction as a demand among schoolchildren forced to stay locked indoors.

Similarly, clean water is also becoming a critical issue. The electricity sector—still the dominant energy source in India—is still largely based on coal, and this sector of India’s economy is one of the largest consumers of the country’s scarce water. Meanwhile, increasing economic growth means that the government must meet the burgeoning power demands of the population. But with the overall total water supply slowly declining and pressing agricultural needs (70 percent of India’s farming output is irrigation-based), there are simply not sufficient water resources for a continued expansion of the coal-power sector.

At the same time, India is genuinely committed to overdelivering on its national contributions to the 2015 Paris Climate Agreement, and locking in a sustained, aggressive reduction in the carbon emissions intensity of its economy. Indeed, India is on track to boast just 2 percent growth in carbon emissions in 2019; the country’s lowest rate of carbon-emissions growth this century, (assisted in part by the slowing economic growth rate).

In tackling air pollution, water scarcity, and the Paris targets, it might appear that India is driving its energy transformation because of domestic environmentalism. But this is not really the case. Finance is the central driver. India is embracing renewables and new energy technologies due to the compelling economic benefits of the rapid expansion of a cheaper electricity supply.

Creating a low-cost electricity supply. In 2017, India’s then-energy minister, Piyush Goyal, introduced online competitive “reverse auctions”—where suppliers can view the current bid and make lower bids if they wish—to win the right to build new renewable energy infrastructure across India. This encouraged each Indian state to compete with others, given that both local and international developers were able to choose sites with the best wind and solar resources. (The Indian states of Gujarat and Tamil Nadu offer some of the best sites in the world.)

The results of these reverse auctions were staggering; companies collectively bid for more capacity than was being auctioned by up to ten times. This high investor interest allowed the government of India to select the lowest-cost bids, ultimately benefitting India’s electricity consumers.

Fearful of missing out, the trend continued in subsequent reverse auctions, with investors bidding aggressively with cheap offers—putting enormous downward price pressure on reverse auction results. This in turn encouraged the state and central governments to encourage this investment boom further, by removing legal and regulatory barriers—lending truth to the adage that the flow of money through a system tends to organize it.

With such powerful forces at work, prices kept dropping. Previously expensive renewable energy prices dropped by some 50 percent over 2017 for both solar and then wind, while investors offered 2.40-3.00 rupees per kilowatt hour. This put domestic renewable energy prices about 20-30 percent below the cost of India’s existing domestic coal-fired power generation costs, and even below the cost of plants powered by imported coal or imported liquified natural gas.

Subsequent reverse auction tenders reconfirmed this situation, highlighting the growing range of investors who wanted to participate in India’s renewables boom. Domestic power companies were all interested, including state-owned enterprises (not too subtly nudged by their government ministers to back this national mission using surplus capital they might have otherwise had to pay out as dividends) and private industry leaders like the massive Adani and Tata Groups. Domestic renewable energy specialists were also bidding. They were often backed by global private equity, and international investors who had jumped aboard as well—such as Japan’s SoftBank, Australia’s Macquarie Group, Goldman Sachs of the US, Singapore’s Sembcorp and Temasek, CLP Power Hong Kong, Finland’s Fortum, and France’s EDF.

The bidding for renewable projects became so frenetic that five leading Indian billionaires wrote a joint letter to the prime minister demanding limits to the injections of foreign capital. They said they could not compete with the flood of international investment that was driving electricity prices down and crowding out India’s domestic giants. The government reluctantly complied, putting a cap of $1 billion per bid per participant. An astonishingly good problem to have! India had been suffering from acute electricity supply shortages for a decade and now it was being overwhelmed with new investment in ultra-low cost electricity supply.

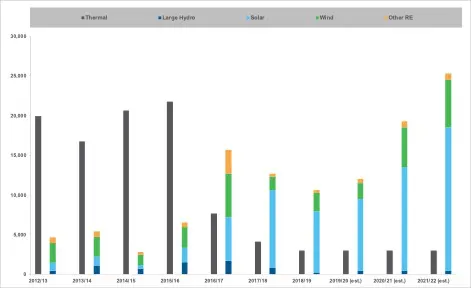

The result? The government of India enabled $40 billion of new investment and a doubling of renewable energy capacity in just over three years, to 83 gigawatts by September 2019, with another 45 gigawatts of large scale hydro-electricity. (To give a sense of scale, the Hoover Dam generates 2 gigawatts.)

Buoyed by the success, India’s initial target of 175 gigawatts of renewable energy capacity by 2022 was expanded to a target of 275 gigawatts by 2027. Then in September 2019, Prime Minister Modi proclaimed a new target of 450 gigawatts by 2030, or another $500 billion of investment in the coming decade.

In addition to low-cost electricity, the government of India had introduced another key benefit into its auction process. Not only were the bids being offered about 20-to-30 percent below the wholesale price of electricity, they were also fixed at a flat rate for 25 years. In doing this, India created a deflationary low-cost electricity system running on zero inflation. A fixed rate is a very material benefit for investors, given consumer inflation was running at 10 percent annually when Modi was first elected Prime Minister in 2014.

India entered the first decade of the 21st-century on a path of massive coal-fired power generation investment, with plans reaching over 600 gigawatts. India now exits this decade with over four-fifths of this high-emission, high-pollution investment intent now shelved, uncompetitive against zero emissions renewable energy.

What’s more, the Indian government’s plans include a progressive expansion of electric vehicles, putting the country on a path to progressively reduce reliance on expensive, high emissions oil imports.

The energy transformation continues despite the economic slowdown. While the Indian government has embraced the deflationary opportunities in renewable energy investment, the technology-driven disruption of its energy system has a long way to go—and it has by no means been entirely smooth sailing.

The national electricity grid is showing signs of serious congestion from the rapid influx of intermittent renewable energy generation. The gold rush for the best wind and solar sites of a few select states has put intense pressure on the grid, created energy distribution bottlenecks, and provoked some policy contradictions—including increased state government charges on renewable energy.

The government of India has also come up against push-back from its domestic manufacturing industry, seeking—and winning—tariff protection from the ever-lower priced solar module imports from China. Prime Minister Modi campaigned on a “Made in India” manufacturing upswing, but the domestic solar industry to-date has been unable to compete with the rapid innovation and huge economies of scale inherent in China’s solar module export industry. The government’s subsequent import duties on Chinese solar modules not only raised solar tariffs by 10-to-20 percent, but caused a 12-to-18 month installation delay as the new rules were all too slowly clarified.

These issues will likely be short-lived, however, as the same imperatives that first triggered this boom continue to remain: to fight the environmental costs of India’s economic growth, and to lower India’s energy costs.

Prime Minister Modi’s target—of ensuring an uninterrupted supply of electricity to all households, industries, and commercial establishments—highlights the government’s well-publicized commitment to transforming India’s electricity system.

The energy security gains of a reduced reliance on fossil fuel imports are clear, as are the benefits of diversifying India’s electricity system from its historic overreliance on heavily polluting coal-fired power generation. And the benefits extend well beyond its borders.

As India benefits from the shift to domestic renewable energy, other emerging market nations are watching, keen to leverage the same benefits for their own countries.

And therein lies a key path to global decarbonization and a much-needed solution to limit global warming.

And none too soon.

Đăng nhận xét